Buildings become vacant for many reasons, including ongoing repairs that make the structure uninhabitable or a tenant moving out. In this case, your standard property insurance policy will create a gap in your coverage.

Vacant building insurance provides specialty coverage for commercial properties that remain unoccupied. Protection is available before you lease out or sell the property.

In this article, we’ll highlight the importance of vacant building insurance and the coverage along with the potential costs.

What is Vacant Building Insurance?

Vacant building insurance protects owners of unoccupied buildings (commercial or residential) from potential hazards such as fire, theft, vandalism, and sprinkler damage. Since vacant property owners are liable for injuries to trespassers and passersby, vacant building insurance includes property owners' liability insurance.

Commercial property is vacant if it has less than 30% square footage occupancy for the intended purpose. The building can be empty for various reasons such as lack of tenants and a change in use of the building.

The property may be a newly constructed and entering the market or retail space in between leases. Vacant insurance policies have specific terms and, for instance, they may require a security monitoring system.

Why is Vacant Building Insurance Needed?

Most standard property insurance policies don’t cover vacant buildings. Typically, if a building remains vacant for 30-60 days, it is excluded from sprinkler damage, theft, and vandalism losses.

Building owners must embrace vacant building insurance to mitigate the financial losses resulting from these risks. A short time lapse is enough to cause significant damage.

Vacant Building Insurance Coverage

Many commercial building insurance policies don't feature extensive coverage for vacant buildings. Therefore, an additional insurance policy is needed to protect your vacant building before you sell it or bring in a tenant.

Vacant building insurance may protect against loss by covering the following events:

- Vandalism and theft: Squatters and vandals can easily access your building and destroy walls, floors, ceilings, fixtures, and equipment. Vacant building insurance covers all forms of deliberate damage on a property, such as fires, glass breakage, defaced walls, and torn-down billboards.

- Debris Removal: Vandals and water damage will leave broken glass, torn down walls, rotten timber, cut-up cables, and dirt on the property. Clearing this waste from your building, especially if it was caused by fire or water damage, might be a difficult task with substantial costs. The expenses for cleaning up dirt and carrying it away from the site are paid for by the insurer.

- Water damage: Sprinkler systems are essential in fighting fire break-outs. However, when faulty, they can cause unintended consequences such as flooding, leading to floor and wall damage. Wet rot, mold, and dry rot are consequences of water leaks. Any damage on the building's walls and floors from water leakage may be eligible for compensation from the insurer.

- Injury to third parties: A building owner is liable for third-party bodily harm that occurs on their property. For instance, a person may be hit by a falling object or sprain their leg from a slippery floor section in the building. Insurance may settle medical, legal, and lost wage expenses.

- Fire department costs: Partial or total loss to the vacant property may occur due to electrical faults. Insurance may cover the fire department service charge (cost to have the fire department respond to the fire).

Under most vacant building insurance policies, there still has to be periodic checking of the building, and an abandoned property without routine monitoring is ineligible for coverage.

How Much Does Vacant Building Insurance Cost?

The cost of the insurance coverage is negligible compared to the cost of a loss.The price of vacant building insurance fluctuates based on the following factors:

- Term: The duration of the vacancy policy can be 3, 6, 9, or 12 months—the greater the length, the higher the cost.

- Length of vacancy: Insurance companies will consider how long the building has been vacant. It may cost more if the vacancy time period is more than three years.

- Location: Most insurance premiums vary based on area. Crime prevalence in specific localities will impact premiums for property insurance against theft and burglary.

- Security systems: A building with a sophisticated security system with real-time alerts and features will have lower premiums than one left unguarded.

- Building size: Premiums increase based on the square footage and floors.

The typical policy coverage limit is $2 million. Some policies offer a $2M occurrence and $3M aggregate.

Key Advantages of Vacant Building Insurance

Vacant building insurance protects against unforeseen risks. For instance, the vandalism of power cables can create short circuits leading to a massive fire in the building, requiring emergency firefighters.

This insurance protects from significant losses. Vacant building insurance may compensate you for theft, vandalism, fire department charges, water damage, property damage, and debris removal.

Vacant buildings might attract vandals, squatters, and thieves. Lack of on-site monitoring exacerbates risks. Also, minor faults such as a damaged sprinkler system or leaky pipes can balloon into problems that cause substantial financial losses.

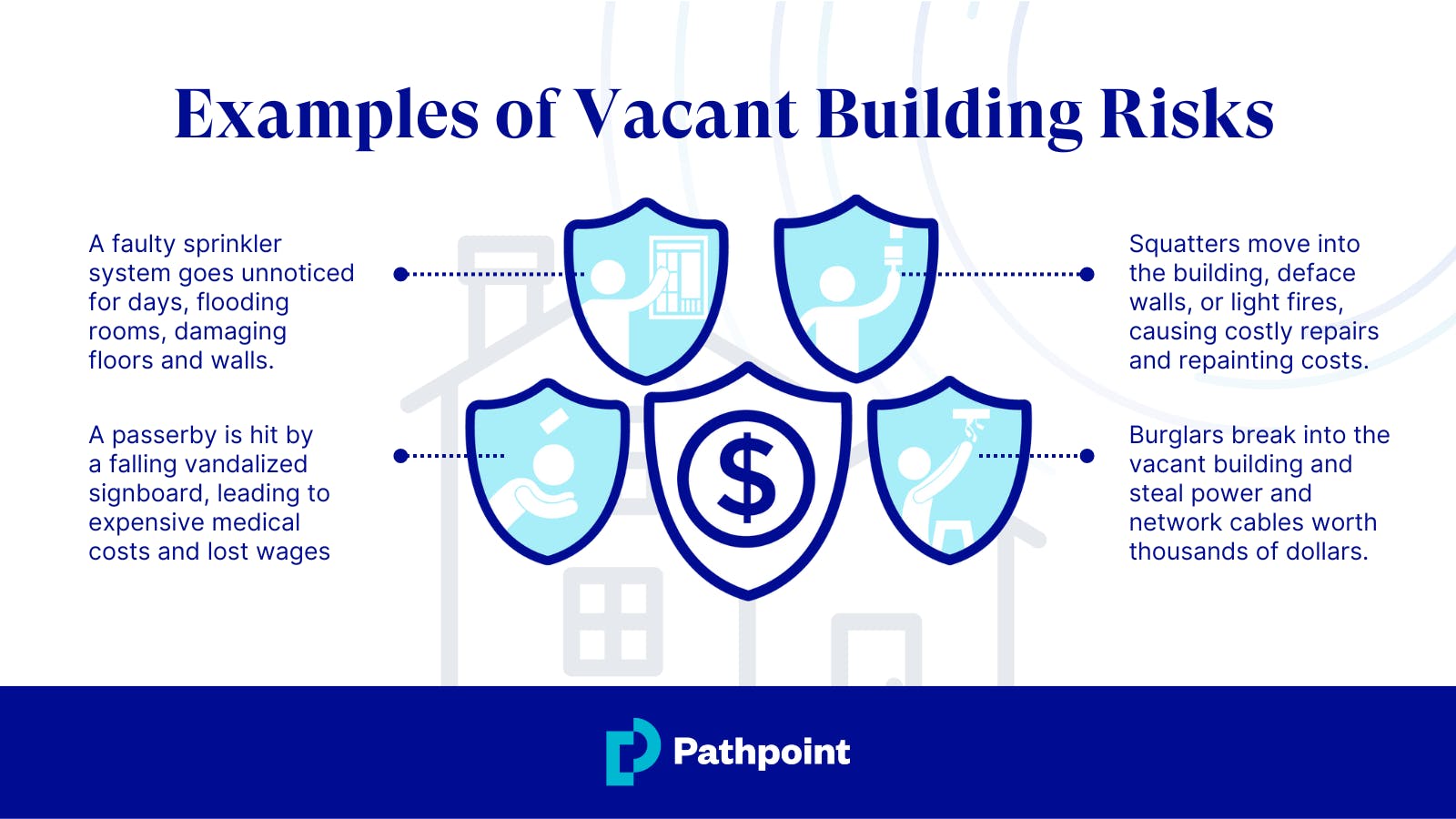

Examples of risks that can arise:

- Burglars break into the vacant building and steal power and network cables worth thousands of dollars.

- Squatters move into the building, deface walls, or light fires, causing costly repairs and repainting costs.

- A faulty sprinkler system goes unnoticed for days, flooding rooms and damaging floors and walls.

- A passerby is hit by a falling vandalized signboard, leading to expensive medical costs and lost wages.

Get Vacant Building Insurance

Get vacant building insurance to protect your investment. Contact your licensed insurance agent and ask them to get you a Pathpoint quote today.